Building on our ultimate guide to life insurance, let’s examine one of the most heavily advertised options targeting older Americans. If you’ve watched daytime TV or browsed senior websites, you’ve seen Open Care life insurance commercials promising “guaranteed acceptance” and “rates never increase.” But what’s the real story? I’ve dug into the policy details, real customer experiences, and industry filings to give you facts over fluff.

What Is Open Care Life Insurance?

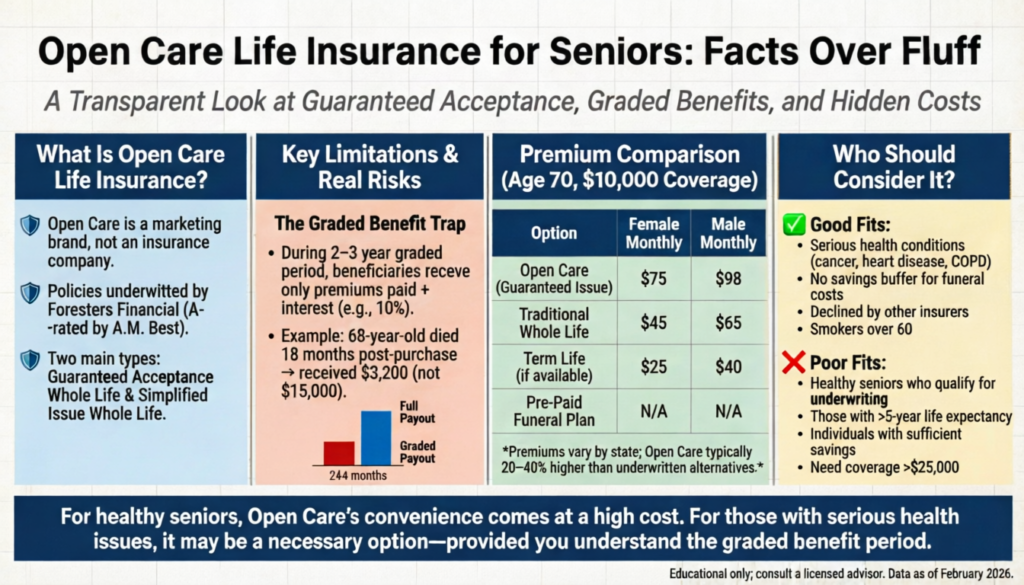

Open Care life insurance is a marketing brand—not an actual insurance company. The policies are underwritten by various carriers, most notably Foresters Financial, an international fraternal benefit society founded in 1874. This distinction matters because your contract isn’t with “Open Care”; it’s with whichever insurer backs your specific policy.

As explained by the III [https://www.iii.org/article/life-insurance], final expense and guaranteed issue products like those sold through Open Care life insurance serve legitimate purposes: covering funeral costs, medical bills, and small debts so families aren’t burdened. However, the marketing often obscures critical limitations that determine whether these policies actually pay out when needed.

How Open Care Life Insurance Actually Works

The Product Structure

Open Care life insurance primarily sells two policy types:

| Policy Type | Underwriting | Death Benefit | Key Limitation |

|---|---|---|---|

| Guaranteed Acceptance Whole Life | No health questions | $2,000-$50,000 | 2-3 year graded death benefit period |

| Simplified Issue Whole Life | Limited health questions | $5,000-$150,000 | Higher premiums for moderate health issues |

NAIC guidance [https://content.naic.org/article/consumer-insight-buying-life-insurance] emphasizes that “guaranteed acceptance” sounds reassuring but comes with trade-offs. During the graded period (typically 2-3 years), if death occurs from non-accidental causes, beneficiaries receive only premiums paid plus interest—not the full face amount.

Real Case: The Waiting Period Trap

A 2023 Florida regulatory complaint involved a 68-year-old woman who purchased Open Care life insurance through a phone solicitation. She died 18 months later from heart failure. Her family expected $15,000 for funeral expenses. Instead, they received $3,200—her premiums plus 10% interest. The graded benefit clause, buried in policy documents she never received in print, excluded full payout until month 24.

The National Association of Insurance Commissioners notes [https://content.naic.org/article/life-insurance-buyers-guide] that graded benefit periods are standard in guaranteed issue products, but marketing materials often emphasize “immediate peace of mind” without clarifying the limitation.

Costs: What You’ll Actually Pay

Premium Reality Check

Open Care life insurance premiums vary by age, gender, and state, but here’s representative 2026 pricing for $10,000 guaranteed acceptance coverage:

| Age | Monthly Premium (Female) | Monthly Premium (Male) | Total Paid Over 10 Years |

|---|---|---|---|

| 50 | $28 | $35 | $3,360-$4,200 |

| 60 | $42 | $55 | $5,040-$6,600 |

| 70 | $75 | $98 | $9,000-$11,760 |

| 80 | $165 | $215 | $19,800-$25,800 |

Bankrate’s analysis [https://www.bankrate.com/insurance/life-insurance/final-expense-insurance/] reveals that Open Care life insurance premiums typically run 20-40% higher than medically underwritten alternatives. For seniors in decent health, simplified issue policies from other carriers often provide better value.

The Break-Even Problem

Here’s the math insurers hope you won’t do: At age 70, paying $98 monthly for $10,000 coverage, you break even at 8.5 years. Live longer? You’ve paid more than the death benefit. Die sooner during the graded period? Your beneficiaries get fractions.

NerdWallet warns [https://www.nerdwallet.com/article/insurance/life-insurance-guaranteed-issue] that guaranteed issue policies make financial sense primarily for those with serious health conditions who cannot qualify elsewhere. Healthy seniors overpay significantly for “peace of mind” they could obtain cheaper through traditional underwriting.

Real Customer Experiences: The Good and Bad

Positive Outcomes

Case Study: The Pre-Planned Funeral

Margaret, 72, purchased $8,000 Open Care life insurance after her husband’s death left her with credit card debt. She selected a policy with Foresters Financial, paid premiums for 4 years, then died unexpectedly. Her daughter received the full $8,000 within 10 days of claim submission—sufficient for cremation and memorial service. The process required only a death certificate and simple claim form.

Foresters’ financial strength (A rating from A.M. Best) ensured claim payment, illustrating that Open Care life insurance works when policies are held long-term and claims are straightforward.

Negative Outcomes

Case Study: The Lapsed Policy

Robert, 69, bought Open Care life insurance through a direct mail solicitation. He set up automatic payments from a checking account he rarely monitored. When he switched banks, payments failed. The grace period notice went to an old address. By the time he discovered the lapse, 4 months had passed. Reinstatement required new underwriting—which he failed due to a recent COPD diagnosis. Two years of premiums ($1,440) were lost; no coverage existed.

Consumer Reports highlights [https://www.consumerreports.org/life-insurance/is-final-expense-insurance-worth-it-a5153665399/] that lapse rates exceed 25% for final expense policies sold through direct marketing channels. Open Care life insurance policies, sold heavily via phone and mail, follow this pattern.

Case Study: The Misrepresented Application

Dorothy, 76, answered “no” to health questions on a simplified issue application, believing her controlled hypertension didn’t count. She died 14 months later. The insurer investigated, found undisclosed hospitalizations, and denied the claim—returning only premiums minus administrative fees. Her children faced $12,000 in funeral costs with no insurance support.

Investopedia explains [https://www.investopedia.com/terms/c/contestability-period.asp] that the two-year contestability period allows insurers to void policies for material misrepresentations. Open Care life insurance applications, often completed hastily over phone, create vulnerability to post-claim disputes.

Open Care Life Insurance vs. Alternatives

| Option | Best For | Cost for $10K (Age 70) | Key Advantage |

|---|---|---|---|

| Open Care life insurance (Guaranteed Issue) | Serious health conditions, need immediate coverage | $75-$98/month | No medical exam, quick approval |

| Traditional Whole Life (Medically Underwritten) | Moderate health, time for underwriting | $45-$65/month | Lower premiums, immediate full coverage |

| Term Life (if available) | Temporary need, excellent health | $25-$40/month | Lowest cost, highest coverage |

| Pre-Paid Funeral Plans | Specific funeral home preference | $8,000-$12,000 lump sum | Price-locks services, no underwriting |

| Savings Account | Disciplined savers, short time horizon | Variable | No premiums, full liquidity |

Forbes advises [https://www.forbes.com/advisor/life-insurance/final-expense-insurance/] that comparing Open Care life insurance against at least three alternatives typically reveals better value for those who qualify for simplified issue. The “convenience” of guaranteed acceptance costs substantially.

Red Flags to Watch

Marketing Tactics

Open Care life insurance advertising emphasizes:

- “No medical exam required” (true, but irrelevant for healthy applicants)

- “Rates never increase” (true for level premium products, but common industry-wide)

- “Benefits never decrease” (misleading—graded benefit periods reduce effective coverage initially)

The Zebra warns [https://www.thezebra.com/life-insurance/guaranteed-issue/] that heavy direct-response marketing often correlates with higher complaint ratios. Check your state insurance department’s consumer complaint database before purchasing.

Agent Practices

Some Open Care life insurance sales occur through call centers with high-pressure tactics. Legitimate concerns:

- Rushing through applications without explaining graded benefits

- Failing to disclose that “final expense” coverage is simply small whole life insurance

- Suggesting cancellation of existing policies to purchase new coverage (often illegal without justification)

Who Actually Benefits?

Good Fits for Open Care Life Insurance

- Ages 50-85 with serious health conditions (cancer, heart disease, COPD) preventing standard approval

- Those needing immediate coverage for funeral expenses with no savings buffer

- Individuals who’ve been declined elsewhere and exhausted alternatives

- Smokers over 60 (smoking penalties often make guaranteed issue competitive)

Poor Fits

- Healthy seniors who could qualify for underwritten coverage

- Those with 5+ years life expectancy who’d pay more in premiums than benefit value

- Individuals with sufficient savings to self-insure final expenses

- Anyone needing coverage exceeding $25,000 (guaranteed issue caps limit utility)

Making the Decision: Practical Steps

- Get medical underwriting first: Apply for simplified or traditional coverage. Declines are free; you’ll know if Open Care life insurance is truly necessary.

- Calculate total cost: Multiply monthly premiums by your realistic life expectancy. Compare to the death benefit. If premiums exceed payout, reconsider.

- Verify the actual insurer: “Open Care” markets policies from multiple carriers. Know who’s backing your contract and their financial rating.

- Understand the graded period: Ask specifically: “If I die of natural causes in year one, what exactly does my beneficiary receive?” Get it in writing.

- Shop competitors: Mutual of Omaha, AARP/New York Life, and Gerber Life offer similar products. Compare premiums and terms directly.

Frequently Asked Questions

Is Open Care life insurance a legitimate company?

Open Care is a marketing organization, not an insurance company. Policies are underwritten by established insurers (primarily Foresters Financial). The products are legitimate but marketed aggressively; the “company” itself doesn’t exist as a legal insurance entity.

Can I be denied Open Care life insurance?

For guaranteed acceptance products, no—hence the name. However, age restrictions apply (typically 50-85). Simplified issue products may decline based on specific health questions.

How quickly does coverage begin?

Accidental death coverage starts immediately. Natural death coverage is graded—typically 2-3 years before full benefit pays. During grading, beneficiaries receive premiums paid plus interest (usually 10%).

Can I cancel Open Care life insurance?

Yes. Whole life policies accumulate cash value slowly; early cancellation means losing most premiums paid. Calculate whether you’ve paid more than beneficiaries would receive before surrendering.

Does Open Care life insurance require a medical exam?

No—this is their primary selling point. However, simplified issue versions ask health questions. Answering inaccurately triggers contestability period investigations and potential claim denials.

How does Open Care compare to AARP life insurance?

AARP partners with New York Life for similar products. AARP often offers better rates for healthier seniors due to group purchasing power. Compare quotes specifically for your age and state—neior is universally cheaper.

What happens if I miss premium payments?

Standard grace periods apply (usually 30-31 days). Lapse means lost coverage and difficult reinstatement, especially if health has declined. Automatic payments help but require monitoring account changes.

Can I increase my coverage later?

Generally no. Guaranteed issue policies lock at initial face amounts. Some carriers allow additional purchases with new applications, but health changes may prevent approval.

Are premiums tax-deductible?

No. Personal life insurance premiums are never tax-deductible. Death benefits are typically income-tax-free to beneficiaries, but this is standard across all life insurance, not unique to Open Care life insurance.

Should I replace an existing policy with Open Care?

Rarely. Replacing in-force coverage triggers suitability reviews and often disadvantages you through new contestability periods and graded benefit resets. Consult an independent advisor before replacing any policy.

The Bottom Line

Open Care life insurance serves a specific niche: seniors with serious health conditions who cannot qualify for underwritten coverage and need immediate, guaranteed funeral expense protection. For this group, the products work as designed—provided policies are maintained long-term and beneficiaries understand graded benefit limitations.

For healthier seniors, the convenience of no medical questions costs thousands in excess premiums. The marketing promises “peace of mind,” but financial peace comes from matching products to actual needs—not from avoiding underwriting that could save you money.

Before committing, explore our complete guide to life insurance types to understand where final expense coverage fits in your broader financial plan. The right policy isn’t the easiest to obtain—it’s the one that pays your beneficiaries maximum benefit for minimum cost.

Educational only; consult advisor. Data as of February 2026.