Why does cheap car insurance for young drivers under 25 feel like hunting for unicorns? If you’re a student, recent grad, or parent of either, you know the sting of those first few quotes. But here’s the good news savings exist if you know where to look.

Table of Contents

Why Is It So Expensive, Anyway?

Let’s rip the band-aid off first. Drivers under 25 pay the highest auto insurance coverage types premiums of any age group. The data is brutal but straightforward—younger drivers file more claims, get into more accidents, and statistically take more risks behind the wheel.

As explained by the III [https://www.iii.org/article/what-determines-the-price-of-my-auto-insurance-policy], age and driving experience are primary factors affecting car insurance premiums. Insurers aren’t punishing you personally; they’re pricing based on decades of accident data. An 18-year-old male might pay 3x what his 35-year-old sister pays for the same vehicle.

But don’t despair. The gap narrows significantly as you approach 25, and there are legitimate ways to bridge it faster.

Finding Cheap Car Insurance for Young Drivers Under 25

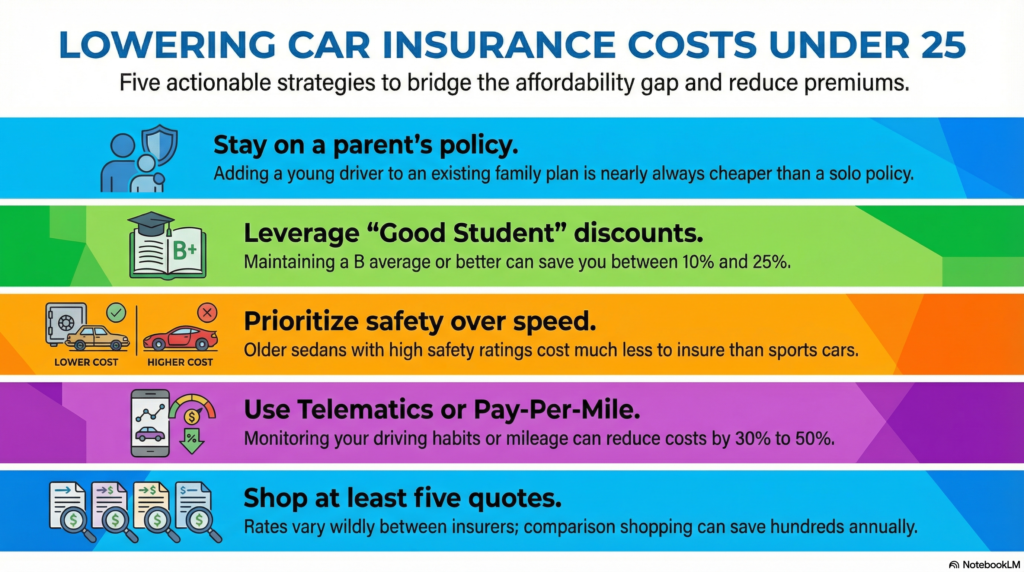

The Multi-Policy Lifeline

Staying on a parent’s policy is usually the cheapest route. NerdWallet confirms [https://www.nerdwallet.com/article/insurance/car-insurance-for-young-drivers] that adding a teen to an existing family plan costs far less than a standalone policy. Yes, the parent’s premium jumps—but that increase is typically smaller than what the young driver would pay solo.

Real talk: I know you want independence. But financial independence means smart choices, not expensive ones. Stay on that family plan through college if possible.

Shop Like Your Money Depends on It (Because It Does)

Rates vary wildly between insurers. Bankrate’s research [https://www.bankrate.com/insurance/car/cheapest-car-insurance-young-drivers/] shows some companies specialize in cheap car insurance for young drivers under 25 while others essentially price them out. Get at least five quotes. Use comparison tools. This one step can save you hundreds annually.

The Vehicle Matters More Than You Think

That 10-year-old sedan? Way cheaper to insure than the sports car you secretly want. Investopedia advises [https://www.investopedia.com/best-car-insurance-young-drivers-5073356] choosing vehicles with strong safety ratings, anti-theft features, and lower repair costs. Insurance companies maintain lists of “youth-friendly” cars—ask your agent.

Car Insurance With College Student Discount

Here’s where being a student actually pays off. Car insurance with college student discount programs are more robust in 2026 than ever, but you have to ask for them.

The Good Student Discount

Maintain a B average or better? Most major insurers offer 10-25% off. Forbes highlights [https://www.forbes.com/advisor/car-insurance/car-insurance-for-college-students/] that this discount applies even if you’re over 21, as long as you’re enrolled full-time. You’ll need to submit transcripts periodically—usually each renewal period.

The Distant Student Discount

Living on campus without a car? The Zebra explains [https://www.thezebra.com/auto-insurance/cheap-car-insurance-college-students/] that many insurers offer “student away at school” discounts. If your permanent address remains with parents but you attend college 100+ miles away, you could see 15-30% reductions. You’re technically still on the policy, just rated as an occasional driver.

University Partnership Programs

Some insurers partner directly with colleges. Check your university’s student services portal—car insurance with college student discount offers sometimes hide in financial aid or student life sections. These partnerships can include perks like waived fees or accident forgiveness.

Smart Strategies Beyond Discounts

| Strategy | Potential Savings | Effort Level |

|---|---|---|

| Defensive driving course | 5-15% | One weekend |

| Telematics/UBI programs | 10-40% | Ongoing monitoring |

| Pay-per-mile insurance | 30-50% for low-mileage | Usage-based |

| Raising deductibles | 15-25% | Financial risk trade-off |

| Bundling renters insurance | 5-15% | Minimal |

Consumer Reports notes [https://www.consumerreports.org/cro/car-insurance/how-to-save-on-car-insurance] that combining multiple strategies often beats hunting for a single magic bullet. A good student discount plus telematics plus a safe vehicle? That’s how you find cheap car insurance for young drivers under 25 without sacrificing coverage quality.

Coverage Decisions That Matter

Young drivers often make expensive mistakes choosing coverage. Here’s what to actually consider:

Don’t Skimp on Liability

State minimums are dangerously low. One serious accident and you could face lawsuits targeting future wages. The NAIC recommends [https://content.naic.org/article/consumer-insight-shopping-auto-insurance] evaluating assets and earning potential when selecting limits—not just current bank account balance.

Comprehensive and Collision

If your car is worth less than $4,000, dropping full coverage might make sense. But calculate carefully. Could you replace the vehicle tomorrow? If not, keep the coverage. The claims process in auto insurance works the same regardless of age, but young drivers file more total-loss claims due to less experience avoiding accidents.

Common Traps to Avoid

“I’ll just drive without insurance.” Don’t. Penalties include license suspension, vehicle impoundment, and SR-22 requirements that make future cheap car insurance for young drivers under 25 literally impossible for years.

“The first quote is fine.” It’s not. I watched a friend accept a $3,200 annual premium when identical coverage cost $1,800 elsewhere. She just didn’t compare.

“I don’t need renters insurance.” Bundling it with auto often costs $10-15 monthly but triggers multi-policy discounts saving $20+ on car insurance. Do the math.

The Road Ahead

Your rates won’t stay high forever. Each year of clean driving helps. By 25, most drivers see significant drops. By 30, if you’ve maintained good records, you’ll wonder why you ever stressed about this.

Until then, be strategic. Leverage every car insurance with college student discount available. Choose vehicles wisely. Drive safely—not just for discounts, but because accidents stay on your record for 3-5 years, compounding the cost of youth.

Frequently Asked Questions

What’s the absolute cheapest way to get car insurance under 25?

Staying on a parent’s policy with multi-car and good student discounts applied. Standalone policies for young drivers rarely compete with family plan pricing.

Do all colleges qualify for student discounts?

Generally, yes—if you’re enrolled full-time at an accredited institution. Online-only schools sometimes face restrictions, so verify with your insurer.

Can I keep my student discount after graduating?

Most good student discounts expire when you lose full-time status or hit age 25, whichever comes first. Some insurers offer recent graduate transitions—ask before you lose eligibility.

Does working part-time affect my rates?

Employment status matters less than how you use the vehicle. Commuting miles impact premiums more than having a job itself. Some insurers offer low-mileage discounts for campus-based students.

Will a parking ticket increase my insurance?

Usually no—parking violations don’t typically affect insurance rates. Moving violations (speeding, running lights) absolutely do, especially for drivers under 25.

Is pay-per-mile insurance good for college students?

Often yes. If you’re on campus most weeks and only drive during breaks, per-mile programs can slash costs dramatically compared to traditional unlimited-mileage policies.

How quickly can I lower my rates?

Immediate steps: shop quotes, apply discounts, adjust coverage. Long-term: maintain clean driving records, build credit, and age into lower risk brackets. Most insurers review driving records every 6-12 months.

Educational only; consult advisor. Data as of February 2026.